this post was submitted on 16 Nov 2024

796 points (98.7% liked)

Microblog Memes

5932 readers

3600 users here now

A place to share screenshots of Microblog posts, whether from Mastodon, tumblr, ~~Twitter~~ X, KBin, Threads or elsewhere.

Created as an evolution of White People Twitter and other tweet-capture subreddits.

Rules:

- Please put at least one word relevant to the post in the post title.

- Be nice.

- No advertising, brand promotion or guerilla marketing.

- Posters are encouraged to link to the toot or tweet etc in the description of posts.

Related communities:

founded 1 year ago

MODERATORS

you are viewing a single comment's thread

view the rest of the comments

view the rest of the comments

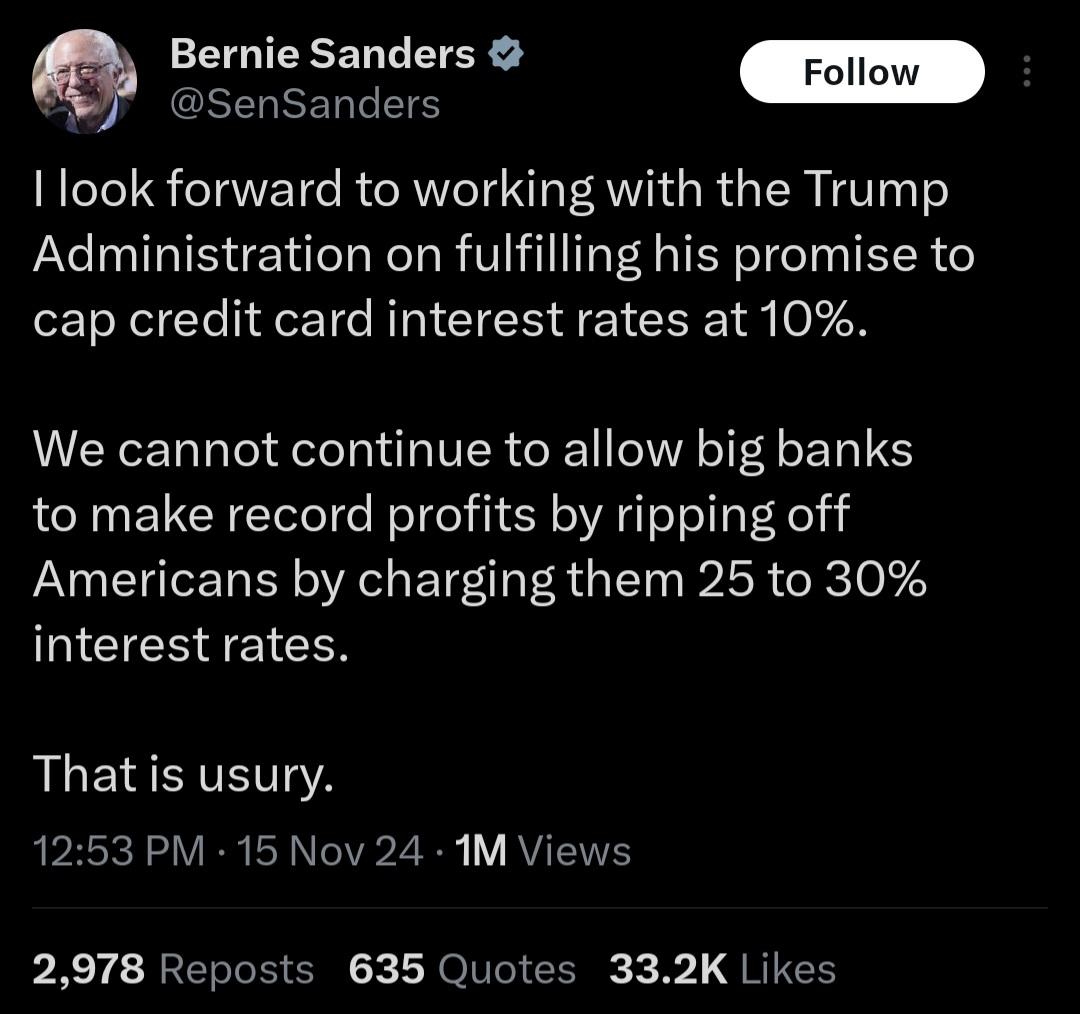

What that would actually mean is a complete lock-out on credit cards for the poor.

Considering how many Americans have crippling credit card debt, especially poor people, would that be worse? I'm sure they'd still offer those credit builder cards with low limits that you have to deposit collateral for the limit.

I'd expect a lot more use of buy now pay later schemes like Klarna.

It's similar to a credit card, but prevents build up of crippling debt.

I personally use my credit card and pay in full each month, not because I need the credit, but because in the UK you get the benefit of Section 75 protection on purchases. I've used that a few times when companies have gone bust. If I'd paid on debit card I'd have been screwed.

Buy now, pay later does not prevent crippling debt. It makes it easy to buy without thinking or realising the actual cost. It makes is easy to stack up invoices that you in the end can't afford.

Don’t Americans have a thing called Credit Score. If you are not paying off debt you don’t build up a score and good luck getting a mortgage without one.

It's a combination of factors. Having debt itself isn't as important as payment history, age of accounts, etc. Credit card debt is probably the opposite of helpful; paying off a card every month in full for a long time is much more useful.

Credit balances don't negatively impact credit scores as much as one would think. It's ultimately a combination of factors that go into an overall credit score with the heaviest hitter being payment history. If one makes all of their payments they can have a decent credit score despite carrying a 10k balance. Carrying a balance of greater than 30% of the limit will detract significantly from the overall score, but it won't knock it below "decent" range on its own.

I'm honestly not even sure how one actually gets their score below 500. My wife got a head injury and physically could not remember whether or not she'd paid her credit cards a couple of years ago, so they ended up becoming delinquent and going to collections. Ultimately it dropped her credit score to about 500 but then it started climbing back up from the car loan and mortgage that are in both of our names and is almost up to 700 again. I seriously want to know how people manage to get their scores down to the 300s (the floor is 300) because you basically have to try in order to get your score that low. A friend of a colleague managed such a feet and then had some identity theft which actually improved his credit score because it looked more like normal credit activity than his real credit activity