Credit Cards

307 readers

1 users here now

A community for discussing any aspect of credit cards. It is important to pay them in full and on time. Please ask questions and contribute to the knowledge surrounding credit cards

Rules

-

No-thing Nefarious. This applies to any posts where we suspect anything potentially illegal or fraudulent, and may include buying/selling tradelines.

-

No Referrals. No links; no codes. Don’t post them; don’t hint at offering them; don’t ask for them. Use rankt.com. This includes any behavior that could be deemed fishing for referrals.

-

No PM’ing Referrals. Spamming other users will get you banned.

-

No Link Shorteners.

-

Self-promotional posts must be pre-approved by a mod. Such posts are generally unwelcome. We may make an exception if it’s truly unique and helpful.

Be nice. (Don’t be a dick.)

founded 1 year ago

MODERATORS

1

2

3

2

Wells Fargo launches the new Autograph Journey Visa, a fresh option that rivals top travel credit cards

(www.businessinsider.com)

4

5

6

5

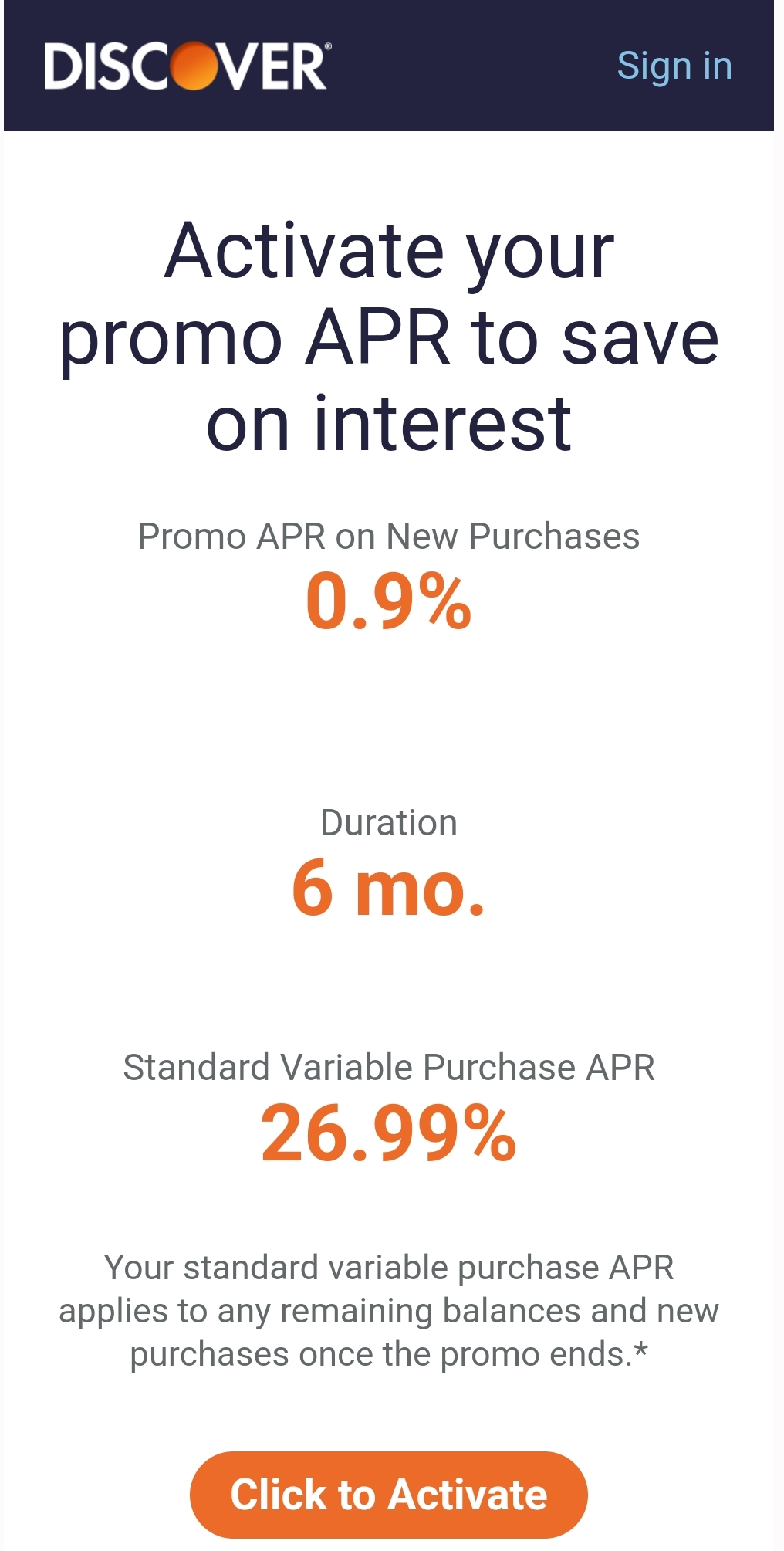

got this email from Discover. I always pay off my bill. is this even worth activating?

(sh.itjust.works)

7

8

9

10

11

12

13

14