this post was submitted on 14 Jun 2023

10 points (100.0% liked)

Investing

799 readers

1 users here now

A community for discussing investing news.

Rules:

- No bigotry: Including racism, sexism, homophobia, transphobia, or xenophobia. Code of Conduct.

- Be respectful. Everyone should feel welcome here.

- No NSFW content.

- No Ads / Spamming.

- Be thoughtful and helpful: even with ‘stupid’ questions. The world won’t be made better or worse by snarky comments schooling naive newcomers on Lemmy.

founded 1 year ago

MODERATORS

you are viewing a single comment's thread

view the rest of the comments

view the rest of the comments

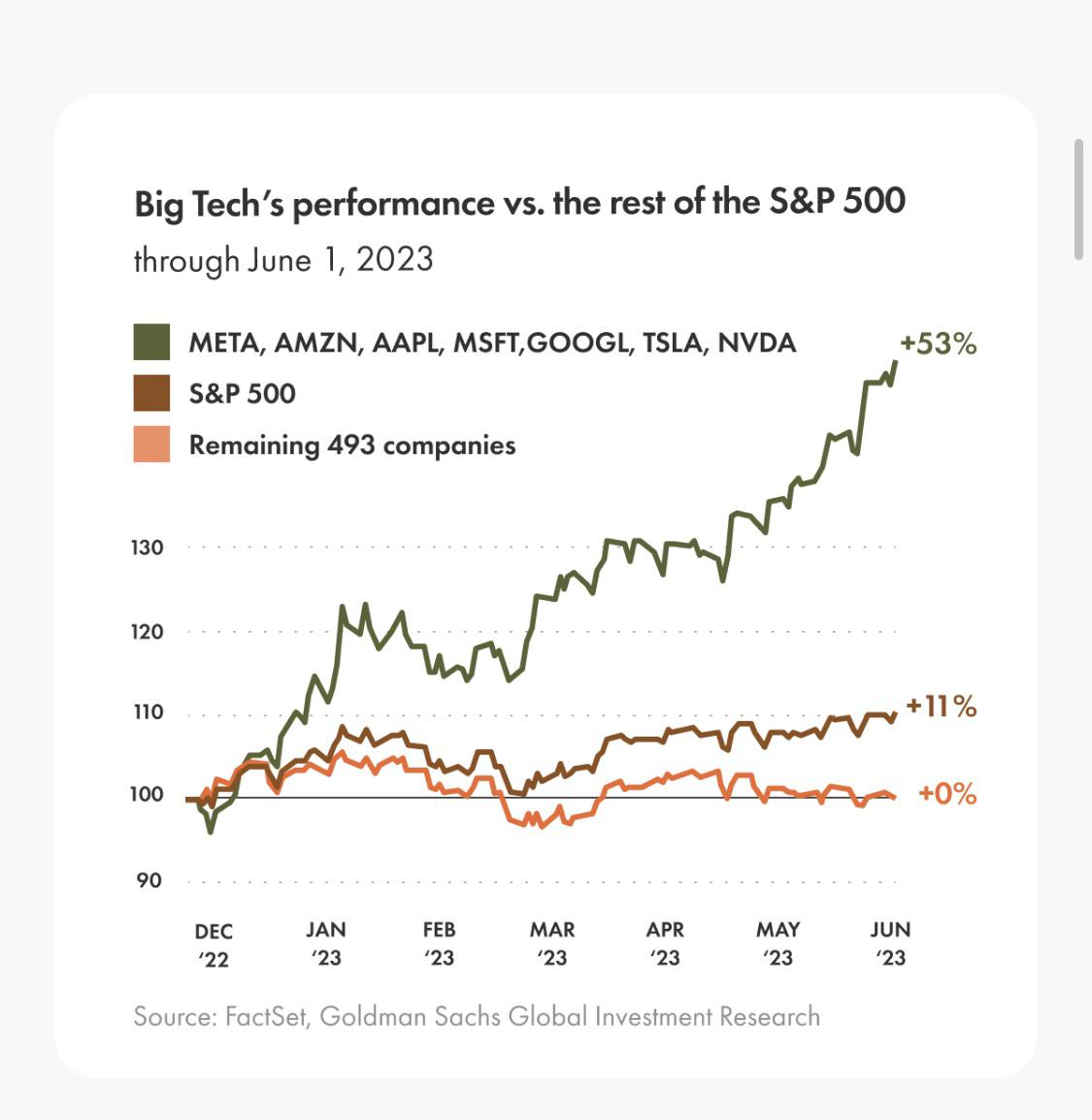

I don't think it's imminent, this isn't really a good indicator.

Capitalism has been working for these companies and they've been centralizing a lot of things to them. The only odd ball here is TSLA, because it's not producing the value it says it does.

I agree on TSLA and I think NVIDIA is highly overvalued. The just make a very specific kind of chips and the AMD and Intel competition will increase in the next months.

Nvidia's fairly consistently been pulling in $2-$4 per share on a TTM (source: https://www.macrotrends.net/stocks/charts/NVDA/nvidia/eps-earnings-per-share-diluted). At $430/share, folks seem to be projecting earnings are going to be about 5-15 times higher over the next decade or two. What seems more likely to me is that, while growth remains strong, growth won't remain 5-15 times higher strong, and the company's going to experience difficulty in leveraging their earnings into higher yields from upstream pricing pressure on the supply chain side, especially if chip foundries are operated in higher cost-of-business countries such as the United States, an embargoed China, or a Mexican city with more expensive access to raw materials.